However depreciation is not deducted from non-current assets directly. It is accounted for when companies record the loss in value of their fixed assets through depreciation. The expense reduces the amount of profit. A depreciation expense reduces net income when the assets cost is allocated on the income statement. PPE Property Plant and Equipment PPE Property Plant and Equipment is one of the core non-current assets found on the balance sheet. When the asset is sold during its useful life the depreciation should be charged for the period the asset is used in the year of sale. In double entry system depreciation expense is determined by dividing the Cost of an asset by the estimated useful life of an asset. Depreciation is an expense which is charged in the current years income statement. The balance in depreciation expense account is transferred to the profit and loss account at the end of the year. Depreciation is instead recorded in a contra asset account namely provision for depreciation or accumulated depreciation.

When the asset is sold during its useful life the depreciation should be charged for the period the asset is used in the year of sale. Calculate how this error would affect Johns Net Profit for the year ended 31 July 2003. Accounting standards does not allow you to expense all the cost of an asset in a one-year profit loss statement. In double entry system depreciation expense is determined by dividing the Cost of an asset by the estimated useful life of an asset. Depreciation is an expense which is charged in the current years income statement. These entries are designed to reflect the ongoing usage of fixed assets over time. Accumulated depreciation is the total amount of depreciation expense allocated to a specific asset. Journal entry for depreciation depends on whether the provision for depreciationaccumulated depreciation account is maintained or not. It is accounted for when companies record the loss in value of their fixed assets through depreciation. PPE is impacted by Capex since the asset was put into use.

Journal Entries for Profit or Loss on Disposal of Asset. When a business has a disposal of fixed assets the original cost and the accumulated depreciation to the date of disposal must be removed from the accounting records. Calculate how this error would affect Johns Net Profit for the year ended 31 July 2003. In double entry system depreciation expense is determined by dividing the Cost of an asset by the estimated useful life of an asset. Depreciation is the gradual charging to expense of an assets cost over its expected useful life. These entries are designed to reflect the ongoing usage of fixed assets over time. Journal entry for depreciation depends on whether the provision for depreciationaccumulated depreciation account is maintained or not. Depreciation expense is an income statement item. There are many methods for calculating depreciation expense but the famous areas. Provision for Depreciation Account which is an expense account used to record depreciation each period An Accumulated Depreciation Account used to show aggregated depreciation The Income Statement Profit and Loss Account The entries are two fold.

PPE Property Plant and Equipment PPE Property Plant and Equipment is one of the core non-current assets found on the balance sheet. A disposal of fixed assets can occur when the asset is scrapped and written off sold for a profit to give a gain on disposal or sold for a loss to give a loss on disposal. Depreciation is instead recorded in a contra asset account namely provision for depreciation or accumulated depreciation. These entries are designed to reflect the ongoing usage of fixed assets over time. Journal Entries for Profit or Loss on Disposal of Asset. PPE is impacted by Capex since the asset was put into use. Both depreciation and amortization are accounting methods designed to help companies recognize expenses over several years. It is the net earnings of a company. In depreciation assets are depreciated to show the true or original value of assets. There are many methods for calculating depreciation expense but the famous areas.

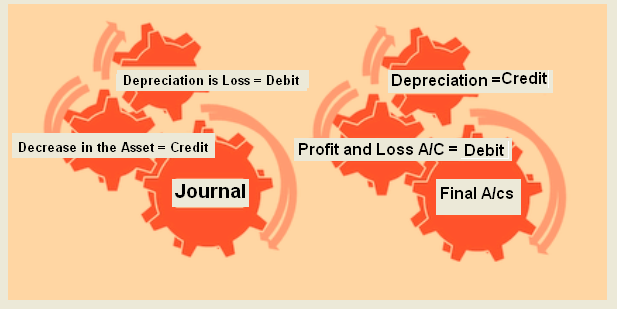

Provision for Depreciation Account which is an expense account used to record depreciation each period An Accumulated Depreciation Account used to show aggregated depreciation The Income Statement Profit and Loss Account The entries are two fold. The value of depreciation is posted to the profit and loss account as expenses. Depreciation expense is an income statement item. The accounting for depreciation requires an ongoing series of entries to charge a fixed asset to expense and eventually to derecognize it. The value of depreciation is deducted from assets value the result gives us the NETBOOK VALUE. Journal entry for depreciation depends on whether the provision for depreciationaccumulated depreciation account is maintained or not. However where the Provision for Depreciation Ac is maintained then the Provision for Depreciation is transferred to the Asset Ac. A depreciation expense reduces net income when the assets cost is allocated on the income statement. B Transfer the profit or loss on disposal to the Profit and Loss account at 30 June. Calculate how this error would affect Johns Net Profit for the year ended 31 July 2003.