Brilliant Related Party Disclosure In Financial Statements Assets Normally Carry A Balance And Are Shown The

Related Party Disclosures Ias 24 Ifrscommunity Com

Related Party Disclosures Objective 1 The objective of this Standard is to ensure that an entitys financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been. RELATED PARTY DISCLOSURES Objective 1 The objective of this Standard is to ensure that an entitys financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been affected by the existence of related parties. Financial statements to assess the potential impact of the related party relationship on the future financial position and performance of the reporting entity. Intragroup related party transactions and outstanding balances are eliminated in the preparation of consolidated financial statements of the group. Where persons are concerned for the definition of a related party step-children are also included within the definition. It helps users of financial statements to detect and explain. If parties become related after the reporting date but before the financial statements are authorised for issue disclosures regarding the new related party may be required in. Information about transactions with related parties is useful in comparing an entitys results of operations and financial position with those of prior periods and with those of other entities. If an entity has had related party transactions during the periods covered by the financial statements IAS 24 requires it to disclose the nature of the related party relationship as well as information about those transactions and outstanding balances including commitments necessary for users to understand the potential effect of the relationship on the financial statements. All amounts received receivable from related parties and all amounts paid payable to related parties as reported in the Income Statement but excluding compensation paid to.

However related party transactions and outstanding balances at reporting date with other entities in the same group are disclosed in the financial statements of the entity only as intra-group transactions and outstanding balances with related party are cancelled out in the preparation of consolidated financial statements of the group.

For each related party disclosed in Note 19 include a separate paragraph presenting the following information. Related Party Disclosures Objective 1 The objective of this Standard is to ensure that an entitys financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been. However related party transactions and outstanding balances at reporting date with other entities in the same group are disclosed in the financial statements of the entity only as intra-group transactions and outstanding balances with related party are cancelled out in the preparation of consolidated financial statements of the group. Its financial statements in accordance with Financial Reporting Standards in Singapore FRS for a number of years. If an entity has had related party transactions during the periods covered by the financial statements IAS 24 requires it to disclose the nature of the related party relationship as well as information about those transactions and outstanding balances including commitments necessary for users to understand the potential effect of the relationship on the financial statements. The Related Party Disclosures Topic provides disclosure requirements for related.

Information about transactions with related parties is useful in comparing an entitys results of operations and financial position with those of prior periods and with those of other entities. Examples of related parties are. 4 Related party transactions and outstanding balances with other entities in a group are disclosed in an entitys financial statements. 31 The value of RPT as disclosed in the financial statements is the aggregate of. The disclosure of related party information is considered useful to the readers of a companys financial statements particularly in regard to the examination of changes in its financial results and financial position over time and in comparison to the same information for other businesses. If parties become related after the reporting date but before the financial statements are authorised for issue disclosures regarding the new related party may be required in. Report all related party transactions that are material to the financial statements. Financial statements to assess the potential impact of the related party relationship on the future financial position and performance of the reporting entity. Related Party Disclosures Objective 1 The objective of this Standard is to ensure that an entitys financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been affected by the existence of related parties. The Related Party Disclosures Topic provides disclosure requirements for related.

A suggestive list includes - Basis of Accounting Transactions involving foreign exchange Investments classification valuation etc Advances and Provisions thereon Fixed Assets and Depreciation Revenue Recognition Employee. Other subsidiaries under common control. Its financial statements in accordance with Financial Reporting Standards in Singapore FRS for a number of years. 4 Related party transactions and outstanding balances with other entities in a group are disclosed in an entitys financial statements. The Related Party Disclosures Topic provides disclosure requirements for related. Purpose of related party disclosures. This publication does not illustrate the requirements of IFRS 4 Insurance Contracts. 31 The value of RPT as disclosed in the financial statements is the aggregate of. Related Party Disclosures Objective 1 The objective of this Standard is to ensure that an entitys financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been affected by the existence of related parties. If an entity has had related party transactions during the periods covered by the financial statements IAS 24 requires it to disclose the nature of the related party relationship as well as information about those transactions and outstanding balances including commitments necessary for users to understand the potential effect of the relationship on the financial statements.

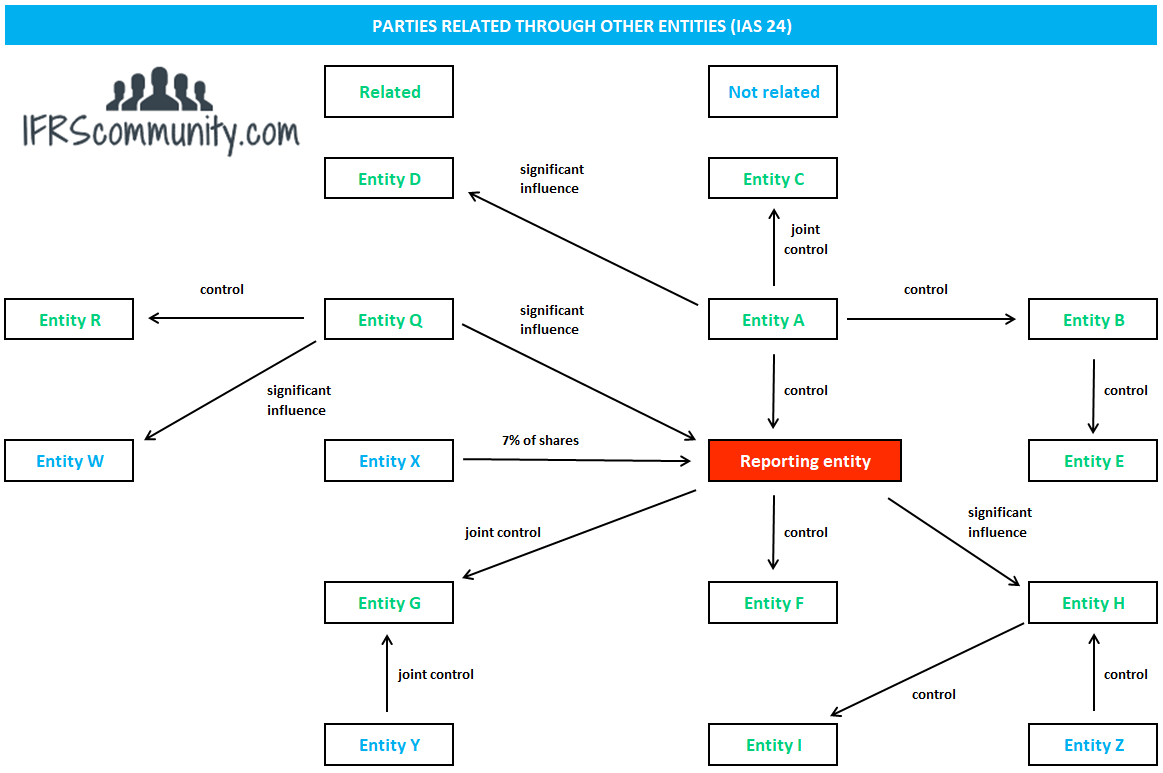

Paragraph 332 says that a related party is a person or entity which is related to the entity that is preparing its financial statements the entity in this case being the reporting entity. Where persons are concerned for the definition of a related party step-children are also included within the definition. FRS 24 revised 2004 Related Party Disclosures FRS 27 revised 2004 Consolidated and Separate Financial Statements FRS 28 revised 2004 Investments in Associates FRS 31 revised 2004 Interests in Joint Ventures FRS 32 revised 2004 Financial Instruments. A description of the nature of the relationship involved including the name of the related party. Related Party Disclosures Objective 1 The objective of this Standard is to ensure that an entitys financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been. 43 Related party disclosures In addition to the subsidiaries included in the consolidated financial statements the KION Group has direct or indirect business relationships with a number of non-consolidated subsidiaries joint ventures and associates in the course of its ordinary business activities. Related Party Disclosures Objective 1 The objective of this Standard is to ensure that an entitys financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been affected by the existence of related parties. The disclosure of related party information is considered useful to the readers of a companys financial statements particularly in regard to the examination of changes in its financial results and financial position over time and in comparison to the same information for other businesses. RELATED PARTY DISCLOSURES Objective 1 The objective of this Standard is to ensure that an entitys financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been affected by the existence of related parties. Purpose of related party disclosures.

The Related Party Disclosures Topic provides disclosure requirements for related. 31 The value of RPT as disclosed in the financial statements is the aggregate of. This publication does not illustrate the requirements of IFRS 4 Insurance Contracts. All amounts received receivable from related parties and all amounts paid payable to related parties as reported in the Income Statement but excluding compensation paid to. However related party transactions and outstanding balances at reporting date with other entities in the same group are disclosed in the financial statements of the entity only as intra-group transactions and outstanding balances with related party are cancelled out in the preparation of consolidated financial statements of the group. However in some jurisdictions parent entity financial information may also be required. RELATED PARTY DISCLOSURES Objective 1 The objective of this Standard is to ensure that an entitys financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been affected by the existence of related parties. Intragroup related party transactions and outstanding balances are eliminated in the preparation of consolidated financial statements of the group. The disclosure of related party information is considered useful to the readers of a companys financial statements particularly in regard to the examination of changes in its financial results and financial position over time and in comparison to the same information for other businesses. Related Party Disclosures Objective 1 The objective of this Standard is to ensure that an entitys financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been.

However related party transactions and outstanding balances at reporting date with other entities in the same group are disclosed in the financial statements of the entity only as intra-group transactions and outstanding balances with related party are cancelled out in the preparation of consolidated financial statements of the group. A suggestive list includes - Basis of Accounting Transactions involving foreign exchange Investments classification valuation etc Advances and Provisions thereon Fixed Assets and Depreciation Revenue Recognition Employee. The disclosure of related party information is considered useful to the readers of a companys financial statements particularly in regard to the examination of changes in its financial results and financial position over time and in comparison to the same information for other businesses. RELATED PARTY DISCLOSURES Objective 1 The objective of this Standard is to ensure that an entitys financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been affected by the existence of related parties. Effective date The illustrative financial statements include the disclosures required by the Singapore Companies Act SGX-ST Listing Manual and FRSs and INT FRSs that are issued at the date of publication August 31 2017. All amounts received receivable from related parties and all amounts paid payable to related parties as reported in the Income Statement but excluding compensation paid to. FRS 24 revised 2004 Related Party Disclosures FRS 27 revised 2004 Consolidated and Separate Financial Statements FRS 28 revised 2004 Investments in Associates FRS 31 revised 2004 Interests in Joint Ventures FRS 32 revised 2004 Financial Instruments. A description of the nature of the relationship involved including the name of the related party. Information about transactions with related parties is useful in comparing an entitys results of operations and financial position with those of prior periods and with those of other entities. 43 Related party disclosures In addition to the subsidiaries included in the consolidated financial statements the KION Group has direct or indirect business relationships with a number of non-consolidated subsidiaries joint ventures and associates in the course of its ordinary business activities.