Fine Beautiful Impairment Of Goodwill Ind As Proprietary Fund Statement Cash Flows

Ias 36 Impairment Of Assets Ppt Video Online Download

Duff Phelps has developed an in-depth understanding of the valuation requirements of ASC 350 as well as the key areas of concern to auditors and the SEC. After initial recognition goodwill and indefinite-lived intangible assets are tested for impairment under ASC 350 at least annually or upon the occurrence of a triggering event. There is no fair value of the goodwill and does not actually bring in anything to the company. Under Ind AS goodwill arises when there is a business combination. For intangible assets with an indefinite useful life or not yet available for use and for goodwill impairment tests are required. The Objective of Ind AS 36 is to ensure that assets are carried at not more than at recoverable value. An impairment charge is a relatively new term used to describe for writing off worthless goodwillThese charges started making headlines in 2002 as companies adopted new accounting rules and. Impairment loss allocation Under IND AS36 impairment loss is first allocated to goodwill in a cash-generating unit with balance allocated over other assets pro- rata. In Ind AS goodwill is not allowed to be amortised. Companies must test goodwill for impairment annually but stakeholders have mixed views about whether this test is effective.

Acquired Internally generated intangibles Under IND AS36 irrespective of an indication of impairment annual impairment.

In Ind AS goodwill is not allowed to be amortised. D For impairment of other financial assets refer to Ind AS 39. Impairment loss allocation Under IND AS36 impairment loss is first allocated to goodwill in a cash-generating unit with balance allocated over other assets pro- rata. Impairment testing requires entities to exercise considerable judgement and there is a need to use. Others say that the test is costly and complex and that impairment losses on goodwill are often reported too late. An impairment charge is a relatively new term used to describe for writing off worthless goodwillThese charges started making headlines in 2002 as companies adopted new accounting rules and.

Some argue that the impairment test informs investors about an acquisitions performance. An impairment charge is a relatively new term used to describe for writing off worthless goodwillThese charges started making headlines in 2002 as companies adopted new accounting rules and. Impairment testing requires entities to exercise considerable judgement and there is a need to use. Since goodwill is not a separate entity or asset it is not possible to conduct an impairment testing for goodwill as an individual asset. After initial recognition goodwill and indefinite-lived intangible assets are tested for impairment under ASC 350 at least annually or upon the occurrence of a triggering event. Therefore all the intangible assets having no finite life are required to be subjected to Impairment testing. The standard also specifies when an entity should reverse an impairment loss and provide disclosures while preparing and presenting the financial statements. IAS 36 sets rules for measuring recoverable amount being higher of assets or cash generating units CGU fair value less costs to sell and its value in use. This standard shall not. Acquired Internally generated intangibles Under IND AS36 irrespective of an indication of impairment annual impairment.

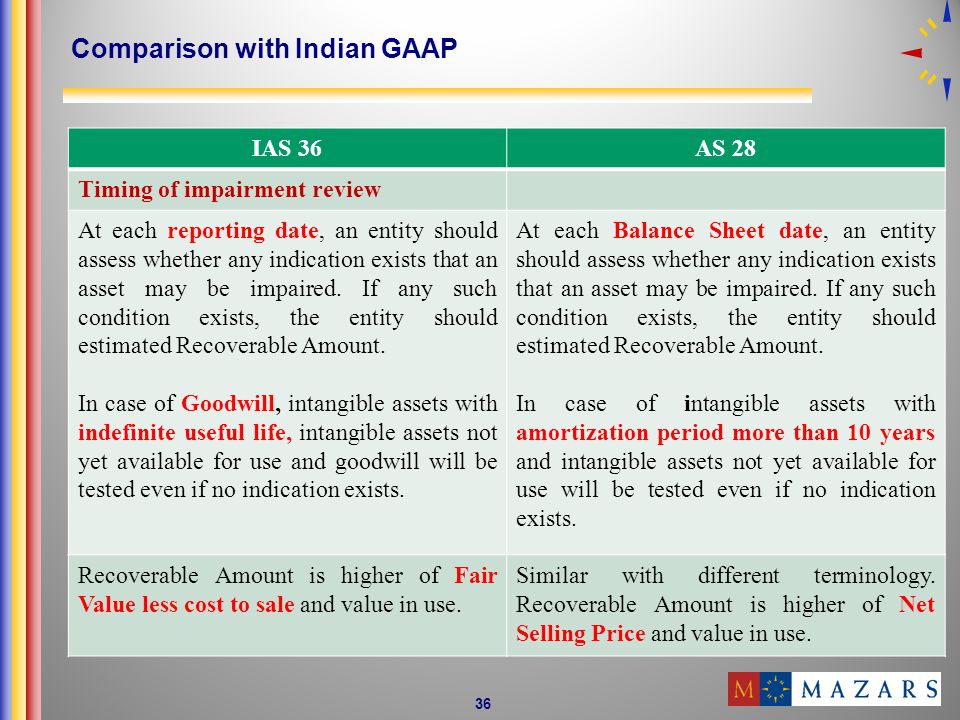

Therefore all the intangible assets having no finite life are required to be subjected to Impairment testing. For CGUs the impairment loss is allocated to goodwill first and then to the rest of the assets pro rata on the basis of the carrying amount of each asset IAS 36104. Impairment loss allocation Under IND AS36 impairment loss is first allocated to goodwill in a cash-generating unit with balance allocated over other assets pro- rata. Disclosure is required for each goodwill impairment loss recognized. Goodwill Impairment it is a deduction from the earnings that companies record on their income statement after identifying that the acquired asset associated with the goodwill has not performed financially as expected at the time of its acquisition. Ind AS 103 prohibits use of pooling of interest method for business combination. As discussed in ASC 350-20-45-2 the aggregate amount of goodwill impairment losses should be presented as a separate line item on the income statement within continuing operations unless a goodwill impairment is associated with a discontinued operation. Under AS28 for allocation of goodwill to a cash-generating unit bottom-up and then top-down test performed leading to differences in measurement. An impairment loss is the amount by which the Carrying Amount CA of an asset or a cash-generating unit exceeds its. The Objective of Ind AS 36 is to ensure that assets are carried at not more than at recoverable value.

Impairment loss except goodwill can be reversed if and only if there has been a change in estimates not because of increase in PV of cash flows as they become closer Increased carrying amount not to exceed the carrying amount that would otherwise exist if no impairment loss had been recognized. Acquired Internally generated intangibles Under IND AS36 irrespective of an indication of impairment annual impairment. Some argue that the impairment test informs investors about an acquisitions performance. As discussed in ASC 350-20-45-2 the aggregate amount of goodwill impairment losses should be presented as a separate line item on the income statement within continuing operations unless a goodwill impairment is associated with a discontinued operation. With the exception of goodwill and certain intangible assets for which an annual impairment test is required entities are required to conduct impairment tests where there is an indication of impairment of an asset and the test may be conducted for a cash-generating unit where an asset does not generate cash inflows that are largely independent of those from other assets. Disclosure is required for each goodwill impairment loss recognized. However the carrying amount of an asset after allocation of the impairment loss cannot decrease below its recoverable amount fair value less cost of disposal or zero. Goodwill should be tested for impairment annuallyTo test for impairment goodwill must be allocated to each of the acquirers cash-generating units or groups of cash-generating units that are expected to benefit from the synergies of the combination irrespective of whether other assets or liabilities of the acquiree are assigned to those units or groups of units. If the total headroom decreases ieTHT1 THT0 it is presumed that there is an impairment of acquired goodwill amounting to THT1THT0unless that presumption is rebutted. After initial recognition goodwill and indefinite-lived intangible assets are tested for impairment under ASC 350 at least annually or upon the occurrence of a triggering event.

An impairment charge is a relatively new term used to describe for writing off worthless goodwillThese charges started making headlines in 2002 as companies adopted new accounting rules and. There is no fair value of the goodwill and does not actually bring in anything to the company. Goodwill Impairment it is a deduction from the earnings that companies record on their income statement after identifying that the acquired asset associated with the goodwill has not performed financially as expected at the time of its acquisition. After initial recognition goodwill and indefinite-lived intangible assets are tested for impairment under ASC 350 at least annually or upon the occurrence of a triggering event. Duff Phelps has developed an in-depth understanding of the valuation requirements of ASC 350 as well as the key areas of concern to auditors and the SEC. The Objective of Ind AS 36 is to ensure that assets are carried at not more than at recoverable value. It is always tested for impairment. Thus it cannot be treated as an individual asset on which you can conduct an impairment testing. Under AS28 for allocation of goodwill to a cash-generating unit bottom-up and then top-down test performed leading to differences in measurement. Impairment loss allocation Under IND AS36 impairment loss is first allocated to goodwill in a cash-generating unit with balance allocated over other assets pro- rata.

There is no fair value of the goodwill and does not actually bring in anything to the company. D For impairment of other financial assets refer to Ind AS 39. Acquired Internally generated intangibles Under IND AS36 irrespective of an indication of impairment annual impairment. Ind AS 103 prohibits use of pooling of interest method for business combination. After initial recognition goodwill and indefinite-lived intangible assets are tested for impairment under ASC 350 at least annually or upon the occurrence of a triggering event. With the exception of goodwill and certain intangible assets for which an annual impairment test is required entities are required to conduct impairment tests where there is an indication of impairment of an asset and the test may be conducted for a cash-generating unit where an asset does not generate cash inflows that are largely independent of those from other assets. Duff Phelps has developed an in-depth understanding of the valuation requirements of ASC 350 as well as the key areas of concern to auditors and the SEC. Goodwill should be tested for impairment annuallyTo test for impairment goodwill must be allocated to each of the acquirers cash-generating units or groups of cash-generating units that are expected to benefit from the synergies of the combination irrespective of whether other assets or liabilities of the acquiree are assigned to those units or groups of units. An impairment loss is the amount by which the Carrying Amount CA of an asset or a cash-generating unit exceeds its. For CGUs the impairment loss is allocated to goodwill first and then to the rest of the assets pro rata on the basis of the carrying amount of each asset IAS 36104.