Outrageous Illustrative Financial Statements Format Of Owners Equity Statement Difference Between Estimated And Projected Balance Sheet

Equity Statement Definition Accounting Equation Line Items

These illustrative financial statements produced by CohnReznick provide examples of private equity financial statements. Notes to the Financial Statements for the financial year ended 31 December 2005 These notes form an integral part of and should be read in conjunction with the accompanying financial statements. See Appendix A for a format illustrating the function of expense or cost of sales method. Following is an illustrative example of a Statement of Changes in Equity prepared according to the format prescribed by IAS 1 Presentation of Financial Statements. Consolidated statement of changes in equity 17. Statement of changes in equity helps users of financial statement to identify the factors that cause a change in the owners equity over the accounting periods. The information contained in these illustrative financial statements is of a general nature relating to private investment companies only and is not intended to address the circumstances of any particular entity. General 12 PwC Holdings Ltd the Company is incorporated and domiciled in Singapore and is publicly traded on the Singapore Exchange. Statement of financial position statement of comprehensive income and statement of changes in equity Examples from IAS 1 IG 6 representing ways in which the requirements of IAS 1 for the presentation of the statements of financial position comprehensive income and statement of changes in equity might be met using detailed XBRL tagging with. Statement of Financial Position 12 Statement of Changes in Equity 13 14 Statement of Cash Flows 15 16 Notes to the Financial Statements 17 104 Appendix A Statement of Profit or Loss and Other Comprehensive Income Illustrating the analysis of expenses by nature 105.

Financial Statements 2019 Example Financial Statements.

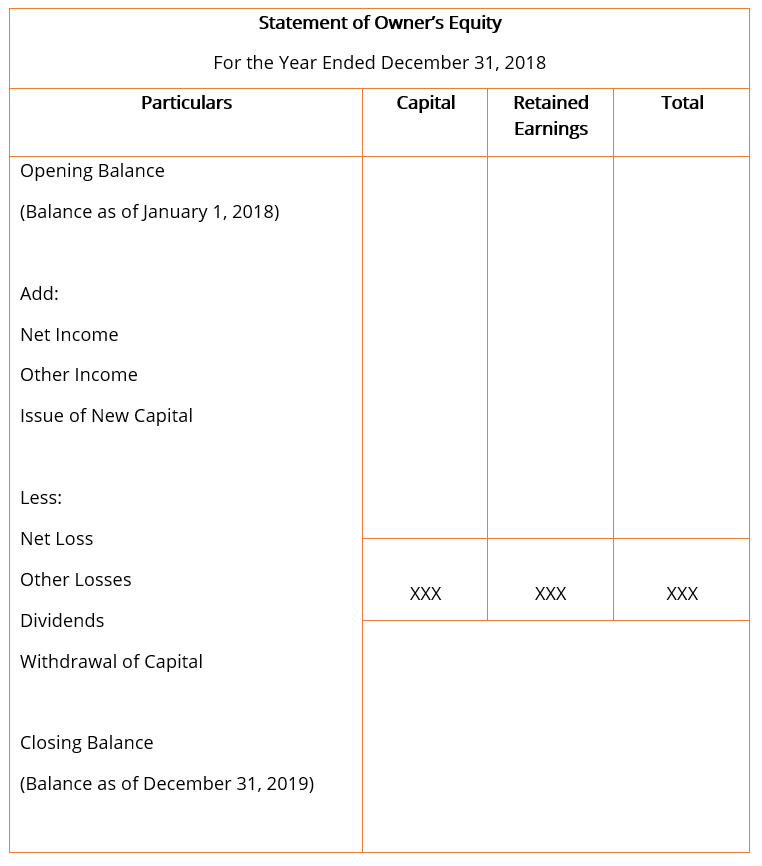

This income statement format illustrates an example of the nature of expense method. Learn how to create an statement of owners equity. These illustrative financial statements which are examples for bank holding companies including community banks thrifts and other financial institutions contain common disclosures as required under US. Statement of financial position statement of comprehensive income and statement of changes in equity Examples from IAS 1 IG 6 representing ways in which the requirements of IAS 1 for the presentation of the statements of financial position comprehensive income and statement of changes in equity might be met using detailed XBRL tagging with. The illustrative financial statements include the disclosures required by the Singapore Companies Act SGX-ST Listing Manual and FRSs and INT FRSs that are issued at the date of publication August 31 2017. Notes to the Financial Statements for the financial year ended 31 December 2005 These notes form an integral part of and should be read in conjunction with the accompanying financial statements.

The example financial statements illustrate a statement of comprehensive income in two statements. The Example Financial Statements are based on the activities and results of Illustrative Corporation and its subsidiaries the Group a fictional consulting service and retail entity that has been preparing IFRS financial statements. Learn how to create an statement of owners equity. Private equity fund managers can use them as a master guide with sample disclosures for common scenarios. Financial Statements 2019 Example Financial Statements. 26 Notes The notes are part of the financial statements and complement the balance sheet the off-balance-sheet the income statement the cash flow statement and the statement of changes in equity. Consolidated statement of changes in equity 17. XI Example disclosures for distributions of non-cash assets to owners 301 XII Example disclosures for government-related entities under IAS 24. Following is an illustrative example of a Statement of Changes in Equity prepared according to the format prescribed by IAS 1 Presentation of Financial Statements. As the only changes to XYZ Groups equity during the year arose from profit or loss and payment of dividends it has elected to present a single statement of comprehensive income and retained earnings instead of separate statements of comprehensive income and.

Illustrative financial statements for Small and Medium-sized Entities SMEs. Presentation requirements are outlined in Annex 4 of the Circular. These illustrative financial statements which are examples for bank holding companies including community banks thrifts and other financial institutions contain common disclosures as required under US. Now constitutes an integral component of the financial statements. Illustrative IFRS consolidated financial statements December 2019 Financial statements 6 Statement of profit or loss 9 Statement of comprehensive income 10 Balance sheet 17 Statement of changes in equity 21 Statement of cash flows 24 Appendices 201 Independent auditors report 200. Statement of financial position statement of comprehensive income and statement of changes in equity Examples from IAS 1 IG 6 representing ways in which the requirements of IAS 1 for the presentation of the statements of financial position comprehensive income and statement of changes in equity might be met using detailed XBRL tagging with. This income statement format illustrates an example of the nature of expense method. Illustrative in nature The sample disclosures in this set of illustrative financial statements should not be considered to be. The Example Financial Statements are based on the activities and results of Illustrative Corporation and its subsidiaries the Group a fictional consulting service and retail entity that has been preparing IFRS financial statements. Statement of changes in partners capital Year ended December 31 20XX General partner Limited partners Total Partners capital beginning of year 75884000 682957000 758841000 Capital.

Illustrative financial statements for Small and Medium-sized Entities SMEs. For listed banks the social and sports fund contribution should be accounted for through the statement of changes in owners equity. ACA Sch 121a the financial statements of the Company are drawn up so as to give a true and fair view of the financial position of the Company as at 31 December 2019 and the financial performance changes in equity and cash flows of the Company for the year then ended. Statement of financial position statement of comprehensive income and statement of changes in equity Examples from IAS 1 IG 6 representing ways in which the requirements of IAS 1 for the presentation of the statements of financial position comprehensive income and statement of changes in equity might be met using detailed XBRL tagging with. Notes to the Financial Statements for the financial year ended 31 December 2005 These notes form an integral part of and should be read in conjunction with the accompanying financial statements. These illustrative financial statements produced by CohnReznick provide examples of private equity financial statements. Private equity fund managers can use them as a master guide with sample disclosures for common scenarios. They can serve as a set of relevant GAAP-compliant examples. Learn how to create an statement of owners equity. GAAP as well as rules and regulations of the US.

Statement of financial position statement of comprehensive income and statement of changes in equity Examples from IAS 1 IG 6 representing ways in which the requirements of IAS 1 for the presentation of the statements of financial position comprehensive income and statement of changes in equity might be met using detailed XBRL tagging with. Notes to the Financial Statements for the financial year ended 31 December 2005 These notes form an integral part of and should be read in conjunction with the accompanying financial statements. Securities and Exchange Commission SEC including financial statement. As the only changes to XYZ Groups equity during the year arose from profit or loss and payment of dividends it has elected to present a single statement of comprehensive income and retained earnings instead of separate statements of comprehensive income and. XI Example disclosures for distributions of non-cash assets to owners 301 XII Example disclosures for government-related entities under IAS 24. Illustrative financial statements for Small and Medium-sized Entities SMEs. These illustrative consolidated financial statements have been prepared on the basis that no financial liabilities have been classified as fair value through profit and loss. Statement of changes in partners capital Year ended December 31 20XX General partner Limited partners Total Partners capital beginning of year 75884000 682957000 758841000 Capital. New standards and amendments are included in the appendices to these illustrative financial statements. The illustrative financial statements include the disclosures required by the Singapore Companies Act SGX-ST Listing Manual and FRSs and INT FRSs that are issued at the date of publication August 31 2017.

This income statement format illustrates an example of the nature of expense method. Illustrative financial statements for Small and Medium-sized Entities SMEs. Presentation requirements are outlined in Annex 4 of the Circular. 26 Notes The notes are part of the financial statements and complement the balance sheet the off-balance-sheet the income statement the cash flow statement and the statement of changes in equity. Notes to the Financial Statements for the financial year ended 31 December 2005 These notes form an integral part of and should be read in conjunction with the accompanying financial statements. Statement of Financial Position 12 Statement of Changes in Equity 13 14 Statement of Cash Flows 15 16 Notes to the Financial Statements 17 104 Appendix A Statement of Profit or Loss and Other Comprehensive Income Illustrating the analysis of expenses by nature 105. Following is an illustrative example of a Statement of Changes in Equity prepared according to the format prescribed by IAS 1 Presentation of Financial Statements. They can serve as a set of relevant GAAP-compliant examples. A single statement presentation is shown in Appendix B. As the only changes to XYZ Groups equity during the year arose from profit or loss and payment of dividends it has elected to present a single statement of comprehensive income and retained earnings instead of separate statements of comprehensive income and.